This is an opinion editorial by Joachim Book, research fellow at the American Institute for Economic Research, and author on All Things Money and Financial History.

All (fiat) money struggles to keep the liabilities of its issuer to its users. In other words, issuers with only some degree of trust or credibility manage to “monetize” some portion of their debt, virtually taking it to others for free. In the extreme, this means that the issuer gets a permanent, non-repayable, interest-free loan with which they can finance a portfolio of assets—the benefits of which they can spend as they please. The most famous example of this is the Federal Reserve Board, and its forfeited profits are sent back to the US Treasury.

Commercial banks do the same, but at the lower layer in the monetary hierarchy. When you’re depositing Fed notes at a commercial bank, you’re leaving a higher level of legal liability for lower-level bank deposits — and you’re financing the bank’s portfolio, with typically zero interest these days. Earning rates.

In the past, commercial banks issued private banknotes (non-interest-bearing liabilities) that could remain in circulation only if their customers decided to keep them, which they did only if they had some convenience in doing so. Got it. For example, British banks of the 1700s and 1800s offered highly embellished notes, proudly displayed their balance sheets and relied on their conservative lending standards, deep-pocketed owners and customers, among other reasons, to pay for their hard earned money. The money was safe. Banks competed for the business of issuing notes, as the notes kept in circulation meant interest-free financing of their assets.

A few steps down in the modern debt-based fiat monetary hierarchy we find a company like Starbucks. Despite not being a bank, it issues money – although a peculiar kind of loan – money. Starbucks has dollar-value stored in outstanding gift cards: the value that consumers essentially paid to the company at zero percent interest. About 6% of the company’s outstanding liabilities are in this form, not in redeemable and repayable dollars, but in coffee (which allows it to evade banking licenses or regulations for money transmitters). For promises of future coffee and/or loyalty rewards, customers are willing to give Starbucks their dollars up front.

This is all to show that the secret of monetary superpowers is to maintain their liabilities to customers.

all money has value because you hold them

While all cryptocurrencies are outside money instead of this inside the money As discussed above trade-fi entities (ie, they are assets, outright owned, Outside Banking system rather than credit claims on an institution like a bank Inside that system), they struggle with a similar problem of obtaining liquidity. For your “crypto” project to be successful, you need to somehow induce customers to hold its tokens – to hand over valuable financial resources in exchange for a stake in its cryptocurrency.

As the most mature and secure cryptocurrency, bitcoin has a major (and distinctly distinct) advantage over every other cryptocurrency: it has control over the money supply, known founder or venture capitalist backers, pre-mines, or any other facility. are not leaders. Which makes cryptocurrencies more like financial securities than the pure monetary assets of bitcoin. people want to hold bitcoin (future) for its use as moneyAnd not for the promise of a loyalty reward or yield or the scandalous pump-and-dump promise of future glory.

Youtube video link.

Every single shitcoin, which includes ETH, fights over available liquidity, and therefore must come up with plans and reasons for its users to keep their (useless) tokens. Check out all the “staking” practices around, where nifty “crypto” projects tap into the illusion of “yield”: if you hold the token today, we’ll pay you More of that token in the future (Ignore dilution and price changes, laugh out loud, Dreaming of untold riches, venture capitalists arrive and hope their funding will allow projects to continue long after millions of users have achieved an organic(-ish) demand for money.

To meet the demand for money, most shitcoin issuers literally bribe their users with newly created or already created tokens – digital weird money with no purpose. Encouraging people to part with real-world value for fake-world shitcoins is the only way they can bootstrap their worthless digital playthings. Some value type, Fool enough people, for a long time, and you could wind your way into a steady, constant rolling-over money demand, interest-free liabilities, or exciting segregation (Q Tether).

Matt Levine writes in Bloomberg:

“Most crypto economics involves some version of ‘if you believe this thing is valuable, then it is valuable’. This is also true in the somewhat looser sense of many other investments, but crypto actually managed it extensively has done.”

That leads to “algorithmic stablecoins”, stablecoins that are not (at a glance) backed by reserves, such as the commercial banks of the free-banking past, but rely on trading arbitrage between the two. Two The crypto project that controls:

“The way you frame it is usually with some sort of Ponzi-ing, because that’s the main way for self-contained crypto projects to create value these days. You say ‘hey if you’re going for dollars’. When you deposit coins, we will pay you a 20% yield in Sharecoins,’ or ‘If you stake Sharecoins we will pay you a 20% yield in Sharecoins,’ or whatever, and the interest rate thereon – at which The rate at which people are given new Sharecoins made out of thin air – high enough that people get excited and do it for trading, even though they think it’s all made up.”

The result is “you ponzi your way to widespread acceptance, and then you maintain value through widespread acceptance, not through an algorithmic peg mechanism.” Incidentally, this is not far from how governments persuade (force) their citizens to accept pieces of waste paper instead of commodity-backed money.

Without a way to replicate the immaculate concept of bitcoin, proof-of-stake chains must compete to issue money by persuading their users to part with valuable assets in exchange for the promise of a larger share of future shitcoin prints. .

In contrast, bitcoin bootstrapped its value from zero by a few users – freely and voluntarily and without any counterfeit promises or financial incentives to hold the tokens – the electricity and computers to validate Block and Mine Bitcoin existed. using hardware.

Russia pretends to be the gold standard and ruble as just another shitcoin

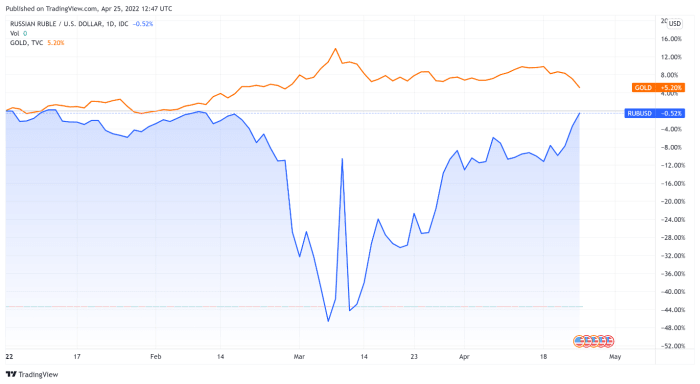

Russia has both set a gold standard in recent weeks, depending on what you believe in, and whose flawed economic framework you follow And ended it. Give it enough time, and I’m sure some clever far-right economist will comment on how this once again illustrates the impracticality of tying money to hard assets like commodities.

One day in late March, officials in Putin’s administration were promising not-so-credulously to buy gold at 5,000 rubles an ounce, allowing the ruble to trade higher against other currencies (albeit with significantly restricted capital flows). ). A few weeks later, as Russia’s currency had strengthened enough to make 5,000 rubles a fair market price for gold, the central bank halted its unilateral pricing of gold. nothing to see here,

When a government promises to tie its currencies to certain assets (currencies of other countries or commodities like gold), its monetary authority is ready to buy sell more at given prices. This policy of pegging one’s currency may be successful if the financial market traders with whom it interacts have trust (credibility), or if the monetary authority has substantial foreign reserve/hard-money assets. Is. If not, sooner or later there are speculative attacks, and the government is forced to mend its ways. Markets can be as brutal as physics.

Source: trading view,

Since the gold announcement, the ruble has reclaimed the level against the USD before the invasion of Ukraine. Why did the gold-backing stunt work?

More likely, it was all a quick-fix credibility game, making the ruble somewhat more desirable to others – if only for transactional purposes. For The Financial Times, Robin Wigglesworth summarizes: “Imports have been crushed, interest rates doubled, strict capital controls imposed, and Russia’s oil and gas sales mean it hoards foreign earnings. continues.” No wonder the ruble is traded more in a much smaller market.

except:

- The gold standard operates on trust: and nobody trusts Vladimir Putin, so there’s little chance it will do much.

- The ruble-gold Play still lacks the redeemability feature that makes up for in true outsized money. BlockFi depositors can redeem their BTC deposits in SAT; Bank of America depositors can withdraw bank money in cash notes outside Bank of America. The holders of the ruble … can not do anything. Redeem them for gold…?

All currencies fight for liquidity and the one tool they use in that fight is to provide their users with a reason to hold their loans or tokens. In that sense, a lot of shitcoins are no different from the ruble, with its issuers desperately trying to ward off counterfeit demand and limit outflows from their monetary networks. Levine again:

“…people don’t trust dollars mostly because you can earn 100% interest on the dollar, or even because you can earn a small amount of interest on the dollar; they trust the dollar because they “Trust the dollar, in a circular, broad-social-adoption way. You don’t have to end up with a Ponzi scheme.”

It is difficult to tell where the ruble, free from internal capital controls and foreign sanctions, will trade against the USD. And it is hard to determine where fiat currencies would trade against hard assets like gold or bitcoin, were they free from government control and taxation.

The circularity of monetary demand is what all currencies want, and the Central Bank of Russia recently showed us some of the shitcoin instruments that produce it. Russian currency may be a step up in respect from shitcoinery, but it is shitcoinary nonetheless. Unlike many of its digital rivals, it has a sizable supply of commodities, natural gas and gold, which it can use to protect its tokens or engineer monetary demand – not to mention the military, bureaucracy and tax system. for.

Sociologist Max Weinrich is believed to have quipped that “a language is a dialect with an army.”

We can say the same about shitcoin and fiat currencies.

This is a guest post by Joachim Buch. The opinions expressed are solely their own and do not necessarily represent those of BTC Inc. either . reflect the thoughts of bitcoin magazine,

{kind=link}